What is a Personal Financial Statement?

A personal financial statement is a document, or set of documents, that provides an individual’s financial position at closing date. It is consist of two sections – a balance sheet section and an income statement section. Although an individual can use more complex personal financial statements. The format defined in our excel template can be a good starting point for individuals who are new to using personal financial statements.

A. Personal Balance Sheet

The balance sheet part of the personal financial statement lists the individual’s assets and liabilities. The simple format of our Excel template can be modified as per an Individual’s requirements. For instance, Bob might have 4 checking accounts, 2 savings accounts, 3 houses, and 3 cars. With a few modifications, the template used by John can also be used by Bob.

B. The Income Statement

Unlike the balance sheet, which lists out all stock variables affecting an individual’s financial position, the income statement lists out all flow variables affecting an individual’s financial position.

Why use a Personal Financial Statement?

A personal financial statement can be a very valuable tool in planning out one’s finances. It is usually goal-oriented and can help an individual reach his or her financial goals, especially for young professionals entering the workforce for the first time. Most of these people are new to financial planning and a simple personal financial statement is an easy place to start.

If you have already created and follow a budget, your PFS is basically half done. A personal cash flow statement is almost exactly the same thing as a budget, except that a budget is a plan or projection, and your cash flow statement lists your actual earnings and expenses.

A cash flow statement helps you create your budget. Your budget helps you plan how you are going to allocate your net cash flow (hoping of course that your net cash flow is positive).

Why use XLSX templates for creating Personal Financial Management?

This spreadsheet allows you to create and update an all-in-one personal financial statement that includes:

- Personal Balance Sheet – for listing assets and liabilities and calculating net worth.

- Cash Flow Statement – for listing all your inflows and outflows and calculating your net cash flow.

- Details Worksheet – for listing individual account balances and the details for your properties and loans.

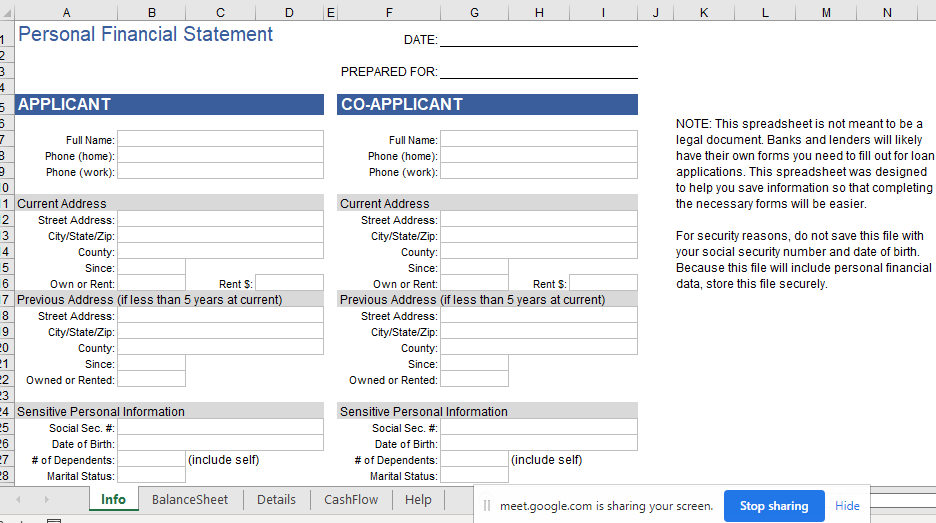

- Info Sheet – for listing contact info that is typically required in loan applications (e.g. names and addresses of the applicant and co-applicant).

It also includes calculations for some common financial ratios:

- Basic Liquidity (BLR) Ratio = Total Liquid Assets / Total Living Expenses : Basic liquidity ratio is a personal finance ratio that calculates the time (in months) for which a family can meet its expenses with its monetary assets. Financial planners and advisers recommend having a minimum basic liquidity ratio of three months.Monetary assets are liquid assets i.e. they are low-or-no risk cash equivalents which can be easily converted to cash with no-or-low loss in value.

- Debt-to-Income (DTI) Ratio = Annual Debt Payments / Annual Income :: A ratio commonly used by lenders to determine how risky of an investment you will be. It should be below about 35% to be considered to have an acceptable level of debt. This comes from the cash flow statement.

- Debts-to-Assets Ratio = Total Liabilities / Total Assets :: Indicates the degree of leverage that is used by a person or company to finance their assets. The higher this ratio the less financial flexibility you have. This comes from the balance sheet.

Why does a Personal Finance help you increase your financial literacy?

Did you already know the relationship between a cash flow statement and a budget? It’s not that the PFS is going to teach you directly. The point is that to accurately complete your personal financial statement you are going to need to ask a lot of questions, and probably do a lot of Google searching, to figure out why such-and-such is a liability, or what exactly is an asset, etc.

Using the template will give you a big head start, but don’t assume that everything I’ve included in the spreadsheet is 100% correct or that it is organized optimally for your needs. Use it as a template – it is just a framework to help you get started. Verify all formulas and make sure you understand exactly how things are calculated.

Importance of Financial Statement in loans application

A lender needs to evaluate the risk of lending money to you. One of the ways they do that is by analyzing your income and how much debt you currently have. They can get that information from your personal financial statement.

If you are applying for loans, banks will likely have their own personal financial statement (PFS) forms for you to fill out (I’ve linked to a couple in the references at the bottom of this page). But, if you are already maintaining your own PFS in Excel, then that will make the process MUCH easier.

How to Create your Personal Balance Sheet?

Step 1: List all your Assets

An asset is something that you own that has exchange value. You may really love your pet rock, but it’s probably not an asset. Your financial assets are your cash, savings, checking account balances, real estate, pensions, etc.

Watch out for the cells that are highlighted gray. These are values that come from the Details worksheet. If you overwrite the formula, you’ll need to fix it.

Click on the links labeled “Schedule 1” or “Schedule 2” to go directly to the spot on the Details worksheet for entering those assets.

Step 2: List all your Liabilities

Liabilities are your debts and other unpaid financial obligations. Future expenses such as fuel for your car are not liabilities, but unpaid bills are.

Step 3: Calculate Net Worth = Assets – Liabilities

The full market value of your home is an Asset. The amount you still owe on the mortgage is a Liability. The difference is what you call call Home Equity. In a typical business balance sheet, the terms Owner’s Equity or Shareholders Equity are the same as Net Worth: Owner’s Equity = Assets – Liabilities.

How to Create Personal Cash Flow Statement?

Step 1: List all your Inflows

Inflows include all sources of income (wages, dividends, etc.) and whatever else puts money in your pocket.

The Inflows are grouped into “Income” and “Other Inflows”, because some financial ratios are based on “Income” and not all inflows are necessarily considered income (such as tax returns, reimbursements, or gifts). You’ll need to decide what should be considered income, perhaps by consulting with your accountant.

If your home or stocks increase in value, there is no cash inflow until you sell them. So, realized capital gains (the profits from the sale of property) are inflows, but unrealized capital gains (the gain in value of unsold property) are not.

Step 2: List all your Outflows

Categorizing your outflows is important if you want to calculate certain financial ratios. For example, the “Payroll Deductions” category consists of things deducted from your paycheck. The net income used by the Debt Service Ratio is your gross income minus these deductions.

Why aren’t insurance premiums listed under payroll deductions? You can list them there if you want to. But, if you didn’t have any income, you would still want to have health insurance, so I find that including health insurance under living expenses is more convenient for calculating the “Total Living Expenses” used by the BLR ratio.

The “Financing Activities” category of outflows is used to determine your total debt payments. That total is used by the debt-to-income ratios. For these ratios, the mortgage payment includes the escrow payment (property tax and insurance) in addition to interest and principal.

Step 3: Calculate Net Cash Flow = Outflows – Inflows

One of the first things you need to learn about personal finance is how to calculate your net cash flow. That is simply the sum of all your inflows (wages, investment income, gifts, and whatever else puts money in your pocket) minus the sum of your outflows (everything that takes money out of your pocket).